Kerala Plus Two Accountancy Chapter Wise Previous Questions Chapter 2 Accounting for Partnership – Basic Concepts

Plus Two Accountancy Accounting for Partnership – Basic Concepts 1 Marks Important Questions

Question 1.

Which of the following is not an item in the profit and loss appropriation account? (June 2010)

a) Interest on capital

b) Salary paid to partner

c) Interest allowed to partner’s loan.

d) None of the above

Answer:

d) None of the above

Question 2.

Find the odd one and state reason, (Say 2011)

a) Interest on Capital

b) Interest on Loan

c) Salary to partners

d) Bonus to partners

Answer:

b) Interest on Loan – Charge againt profit – All others are appropriation of profit.

Question 3.

Which of the following account is credited with inter-est on capital under fixed capital method? (March 2012)

a) Profit and Loss Appropriation Account.

b) Profit and Loss Account

c) Capital Account

d) Current Account

Answer:

d) Current Account

Question 4.

Partners Salary is debited to a/c (Say 2013)

a) Trading

b) Profit and Loss

c) Capital

Answer:

d) Profit and Loss Appropriation p d. Profit and Loss Appropriation a/c

Question 5.

In the absence of any agreement partners will share profit and losses in the ratio. (Say 2013)

a) Gaining

b) Equal

c) Sacrificing

d) Capital

Answer:

b-Equal ratio

Question 6.

Under fixed capital method, interest on drawings is debited in A/c. (March 2016)

Answer:

Partner’s current A/c

Question 7.

What is the journal entry to be passed for transferring partners salary to partner’s capital account? (March 2016)

Answer:

Partner’s salary A/c Dr To partner’s capital A/c

Question 8.

If partners are entitled to interest on capital as per agreement, such interest is payable (Say 2016)

a) Only out of bank balance

b) Only out of capital

c) Only out of profits

d) Only out of sales

Answer:

c) Only out of profits

Question 9.

Firoz and Shahin are partners in a firm. The firm did not have any partnership deed. Specify how the following situations are treated. (March 2017)

a) Sharing of profit and losses.

b) Interest on advance given by Firoz to the firm.

Answer:

a) Profits and losses are to be shared equally among partners.

b) Firoz is entitled to get an interest of 6% p.a.

Question 10.

Partners capital account and current account are not maintained separately under ………………. method of maintaining capital account. (March 2017)

Answer:

Fluctuating capita method

Plus Two Accountancy Accounting for Partnership – Basic Concepts 2 Marks Important Questions

Question 11.

Partner of a firm withdraw Rs. 6,000/- during the year. The accountant changed Rs, 300/- as interest on the same at 10% rate of interest. If it correct? Show the calculation. (June 2009)

Answer:

Correct

Interest on drawings = Amount of drawings x Rate of interest x 6/12

= 6000 x 10/100 x 6/12 = 300

Assumption : The date of drawings is not given. In such case the interest should be 6 months on the whole of the amount.

Question 12.

Analyse the following table and fill up the blank columns: (March 2010)

| Basis of Distinction | Drawings against profit | Drawings against capital |

| 1) Where debited | (a) ? | To capital account |

| 2) Part | Part of the expected profit | (b) ? |

| 3) Effect | (c) ? | Reduces capital |

| 4) Interest | (d) ? | Considered to calculate interest on capital |

Answer:

a) Drawing

b) Part of capital

c) Reduces Profit

d) Considered to calculate interest on drawing

Question 13.

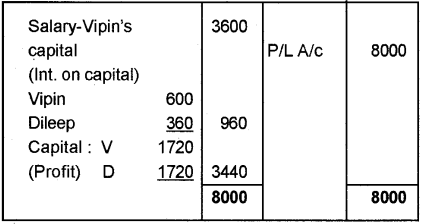

Dileep and Vipin are partners. Dileep’s capital is Rs. 10,000 and Vipin’s capital is Rs. 6,000. Interest is payable @ 6% p.a. Vipin is entitled to a salary of Rs. 300 per month. Profit for the current year before interest and salary to Vipin is rs. 8,000. Divide the profit between Dileep and Vipin. (March 2009)

Answer:

P & L Appropriation A/c

Question 14.

Anu, Minu & Sinu are in Partnership with a profit sharing ratio of 2:1 :1, but Sinu is given a guarantee to get a minimum profit of Rs. 20,000/. During the year the firm get a net profit of Rs. 1,00,000/- then what will be the share of profit due to Sinu? (June 2009) (Say)

Answer:

A:M:S = 2:1:1

Guaranteed amount of profit = 20,000

Net Profit = 1,00,000

Sinu’s share = 1/4 = 1,00,000x 1/4 = 25,000

Sinu should get her actual share of profit ie.

Rs. 25,000. Since her actual share of profit is more than the guaranteed amount of Rs. 20,000/-.

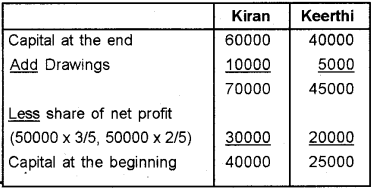

Question 15.

Kiran and Keerti are partners sharing profits in the ratio 3:2. Their capital accounts as on the closing date of the year was Rs.60,000 and Rs.40000 respectively. During the year they made a net profit of Rs.50,000, it was subsequently found that the interest on capital entitled to the partners @ 6% per annum is omitted to record in the books. During the year they withdrew Rs.10000 and Rs.5000 respectively. Find the amount of interest on capital. (June 2010)

Answer:

Calculation of opening capital

Interest on capital

Kiran = 40000 x 6/100 = 2400

Keerthi = 25000 x 6/100 = 1500

Question 16.

A, B & C are partners haring profits and losses in the ratio of 3:2:1 arid their Profit and Loss A/c showed a credit balance of Rs. 24,000. But, on 1st July of the same yearthey decided to share profits and losses equally. What adjusting entry need be made to make necessary effect without closing the profit and loss account? (Say 2011)

Answer:

| C’s Capital A/c Dr To A’s Capital A/c (P & L are adjusted) | 4,000 | 4,000 |

Question 17.

Prasanth and Janish are partners. They do not have any partnership agreement. What should be done in the following cases? (Say 2016)

i) Prasanth spends twice the time that Janish de-votes to business. Prasanth claims that he should get a salary of?3,000 per month for his extra time spent.

ii) Prasanth wants to introduce his son Shenoi as a partner. Janish objects to it.

Answer:

i) No salary will be paid to Prasant

ii) Shenoi will not be admitted as a partner

Plus Two Accountancy Accounting for Not For Profit Organisation 3 Marks Important Questions

Question 18.

What is a Partnership Deed? Give any four items to be included in it. (March 2016)

Answer:

Partnership deed is a written document which contains the rules and regulations regarding the conduct of business.

Contents of partnership deed:-

- Name and address of the firm

- Name and address of partner

- Nature of business

- Duration of partnership

- Capital contributions

Question 19.

Anwar a partner in Akbar Travels withdraw money during the year ending 31st (March 2016) from his capital account for his personal use. Calculate interest on drawings on the following situations if rate of interest is 9% p.a.. (March 2017)

a) If he withdrew Rs. 2,500 per month at the begin-ning of the month.

b) If the amount withdrawn were on 1-6-2015, Rs.7,500, on 31-8-2015 Rs. 3,000 and 30-9-2015 Rs. 6,500

Answer:

a) Total amount withdrawn by Anwar = 2500 x 12 = 30,000

Interest on drawings = Total drawings x Rate x Average Period

Average period = \(\frac { 12+1 }{ 2 } =6.5\) months Interest on drawings

= 30,000 x \(\frac { 9 }{ 100 }\) x \(\frac { 6.5 }{ 12 }\) = 1462.50

b)

| Date | Amount of Drawings | Months for which interest to be charged | Product |

| 01-6-2015 31-8-2015 30-9-2015 | 7500 3000 6500 | 10 (June to March) 7 (Sept. to March) 6 (October to March) Total | 75,000 21,000 39,000 |

| 1,35,000 |

Interest on drawings = 1,35000 x \(\frac { 9 }{ 100 }\) = 12,150

Interest for one month = 12,150 x \(\frac { 1 }{ 12 }\) = 1012.50

Plus Two Accountancy Accounting for Not For Profit Organisation 5 Marks Important Questions

Question 20.

Alim and Methew made a serious discussion about the possibilities of starting a bakery shop as a partnership firm. Alim pointed out several peculiar features that their business should have. Mathew insisted for a written partnership deed and put forward _ some contents to be included in it. Imagine their discussion: (March 2009)

(a) Write two points raised by Alim.

(b) Justify Mathew’s argument.

Answer:

(a) 1) Partnership is the relation between two or more persons.

2) Partnership are governed by Indian Partnership Act, 1932.

(b) Partnership deed is a written document containing the rules and regulations regarding the conduct of business. It contains.

- Name and address of the firm

- Names and addresses of partners

- Duration of Partnership

- Nature of business

- Salary, commission etc. payable to partners

- Profit-sharing ratio

Question 21.

Zeema and Neemsa are partners from 1st Jan, 2008 without partnership agreement and they introduced capitals of Rs. 70,000 and Rs. 40,000 respectively. On 1st July, 2008 Zeema advances Rs. 15,000 by way of loan to the firm without any agreement as to interest. The profit and loss account for the year 2008 discloses a profit of Rs. 16,450, but the partners cannot agree upon question of interest or upon the basis of division of profits. You are required to divide the profit between them giving reasons for your method. (March 2010)

Hint: Prepare Profit and Loss Appropriation Account.

Answer:

Profit as per P/L a/c – Rs. 16450

Less: interest on loan to the firm (15000 x 6/100 x 6/12) – Rs. 450

Actual Profit – Rs. 16000

Zeema’s share of profit = 16000 x 1/2 = 8000

Neema’s share of profit = 16000 x 1/2 = 8000

If any partner has given a loan to the firm is addition to his/her share capital, he/she shall be entitled to

interest on such loan @ 6% p.a. Such interest shall be paid even if the firm making any profit. If there is no written agreement, profits and losses are to be shared equally among partners.

Question 22.

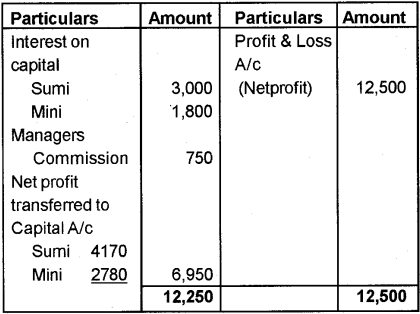

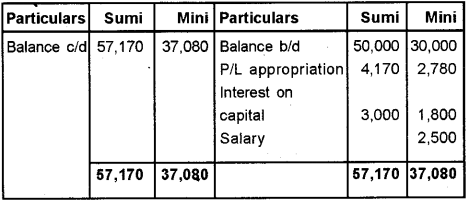

Sumi and Mini are partners sharing profits in the ratio of 3: 2. Their capital stood at Rs. 50,000 and Rs. 30,000 respectively. As per the deed interest on capital is payable at 6% p.a. Mini is entitled to an annual salary of Rs. 2,500. The firm has reported a profit of Rs. 12,500 before charging interest on capital but after charging Mini’s salary for the year ending on 31-03-2009). (March 2011)

Towards Manager’s Commission a provision of 5% is to be made.

Prepare P & L Appropriation Account and partner’s Capital A/c.

Answer:

Profit and Loss Appropriation A/c

Capital A/c

Question 23.

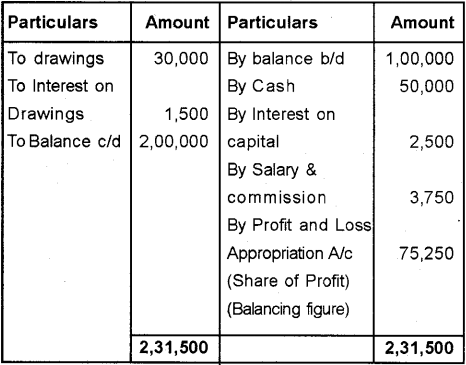

Using the following information prepare the Capital Account of Sri. Ganesh and find out his share of profit. (March 2012)

Capital on 1 -4-2009. Rs. 1,00,000

Capital on 31-3-2010. 2,00,000

Drawings during the year 30,000

Interest on drawings 1,500

Additional capital introduced 50,000

Interest on capital 2,500

Salary and commission 3,750

Answer:

Ganesh’s Capital A/c

Question 24.

P, Q and R are partners in a firm sharing profits/ losses in the ratio of 5:3:2. But R is guaranteed with a minimum amount of Rs. 15,000/- as his share of profit every year. Any deficiency arising on that account shall be met by Q. The profits for the 2 years ending on 31st December 2008 and 2009) were Rs. 60,000 and Rs. 90,000 respectively. (March 2012)

Prepare Profit and Loss Appropriation Account for the two years.

Answer:

Profit and Loss Appropriation A/c for the year 2008 & 2009)

Note:

P’s Share of profit in the year 2008 – 60000 x 5/10 = 30000

P’s Share of profit in the year 2009) – 90000 x 5/100 = 45000

Q’s Share of profit in the year 2008 – 60000 x 3/100 = 18000

Less : Guaranteed amount 15000, 3000

Q’s Share of profit in the year 2009) – 90000 x 3/100 = 27000

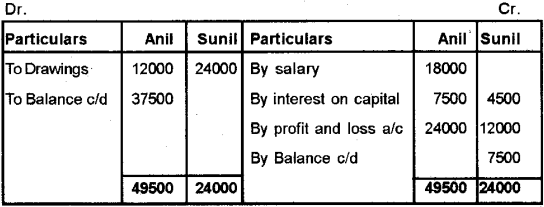

Question 25.

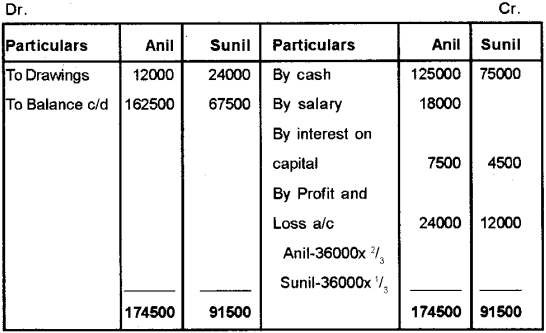

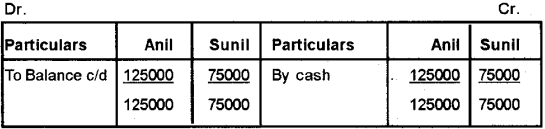

Anil and Sunil commenced business as partners on 1st April 2008. Anil contributed Rs. 125000 and Sunil contributed Rs.75000 as their share of capital. The partners decided to share profits and losses in the ratio of 2:1. Anil was entitled a salary of Rs.1500 per month. Interest on capital was to be provided @ 6% p.a. (June 2012)

The drawings of Anil and Sunil forthe year ending 31st (March 2009) were Rs. 12000 and Rs.24000 re-spectively. The profits of the firm after providing for Anil’s salary and interest on capital were Rs.36000. Draw up the capital accounts of the partners when;

a) Capital are fluctuating

b) Capital are fixed.

Answer:

a) Capital are fluctuating

Partner’s Capital A/c

b) Capital are fixed

Partner’s Capital A/c

Partner’s Current A/c

Question 26.

Arya and Meera are partners. They do not have any partnership agreement. What should be done in the following cases? (March 2013)

a) Arya wants to introduce her son Hari into the business. Meera objects to it.

b) Meera wants that profits should be distributed in the ratio of capitals but Arya wants that it should be distributed equally. Give reasons for your answer.

Answer:

a) Hari will not be admitted as a partner. According to the Indian partnership Act, a new partner can be admitted into the firm only with the consent of all the existing partners unless otherwise agreed upon.

b) Profit will be distributed equally.

Reason:- In the absence of any written agreement between partners, the profits and losses will be shared equally.

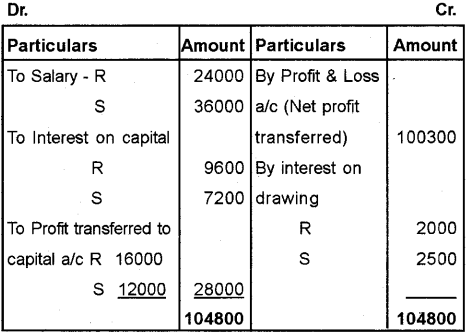

Question 27.

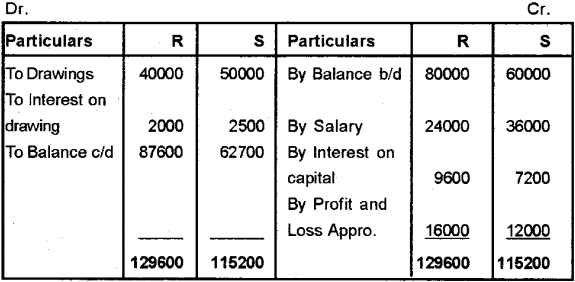

R and S started business on 1st January 2009). On first January 2012), R had a capital balance of Rs.80000 and S had Rs.60000 as capital. According to partnership deed interest on Capital and drawings are 12% and 10% respectively. R and S are to get Rs.2000 and Rs.3000 as salary per month.The profits for the year ending 31st December 2012) before making the above appropriation was Rs. 100300. Drawings of R and S were Rs.40000 and 50000 respectively. Interest on Drawings amounted to Rs.2000 for R and Rs.2500 for S. Prepare Profit and Loss Appropriation Account and Capital Accounts assuming the Capitals are fluctuating. Profits are shared in the ratio 4:3. (Say 2013)

Answer:

Profit and Loss Appropriation A/c

Capital A/c